Interest rate floors are utilized in derivative.

Interest rate cap floor straddle.

An example of a cap would be an agreement to receive a payment for each month the libor rate exceeds 2 5.

Time 0 5 6 004 0 470 4 721 0 021 35 0 06004 0 04721 0 470 0 021 ir modeling a capped floater consider an investor holding a 2 year.

This financial instrument is primarily used by borrowers of floating rate debt in situations where short term interest rates are expected to increase.

Interest rate cap and floor an interest rate cap is a derivative in which the buyer receives payments at the end of each period in which the interest rate exceeds the agreed strike price.

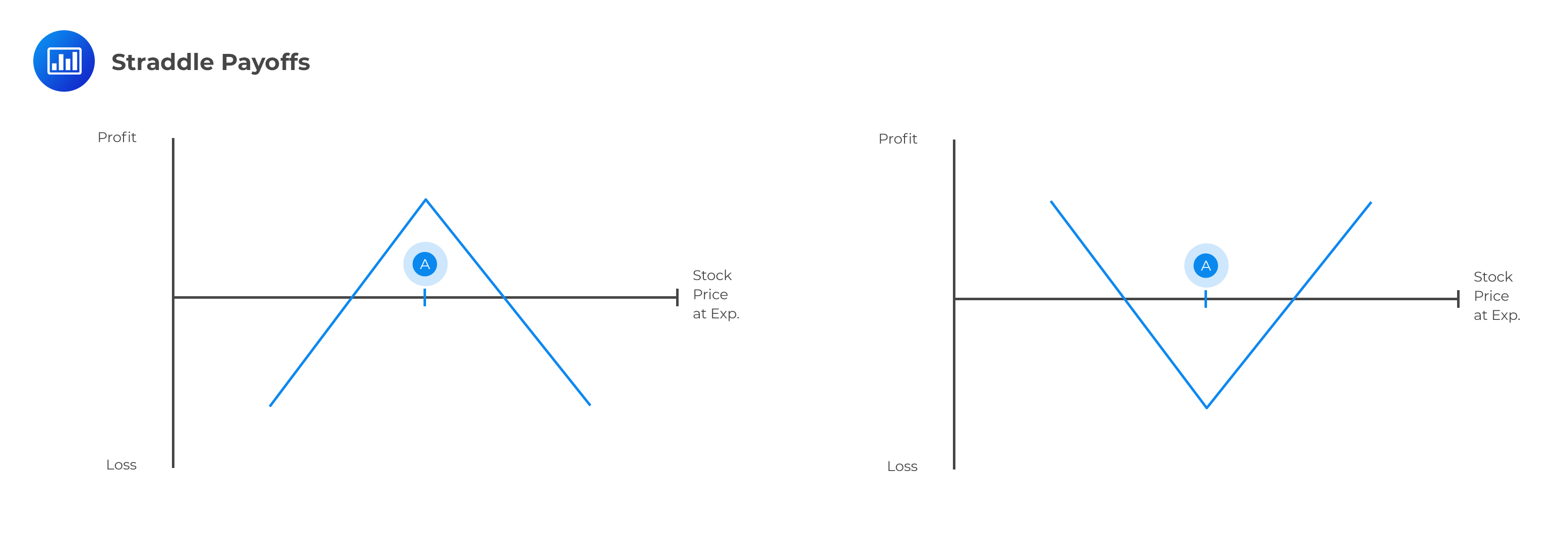

An overview straddles and strangles are both options strategies that allow an investor to benefit from significant moves in a stock s price whether the stock moves up or down.

Therefore it is a bearish position in the bond market.

Similarly an interest rate floor is a derivative contract in which the buyer receives payments at the end.

Interest rate caps and floors are option like contracts which are customized and negotiated by two parties.

An interest rate floor is an agreed upon rate in the lower range of rates associated with a floating rate loan product.

An interest rate cap or ceiling is an agreement between the seller or provider of the cap and a borrower to limit the borrower s floating interest rate to a specified level for a specified period of time.

Caps and floors are based on interest rates and have multiple settlement dates a single data cap is a caplet and a single date floor is a floorlet.

Indeed its interest rate delta is negative.

An interest rate cap is a type of interest rate derivative in which the buyer receives payments at the end of each period in which the interest rate exceeds the agreed strike price an example of a cap would be an agreement to receive a payment for each month the libor rate exceeds 2 5.

:max_bytes(150000):strip_icc()/understandingstraddles2-c0215924b5ba43189e1a136abc5484bf.png)

/10OptionsStrategiesToKnow-02_2-8c2ed26c672f48daaea4185edd149332.png)